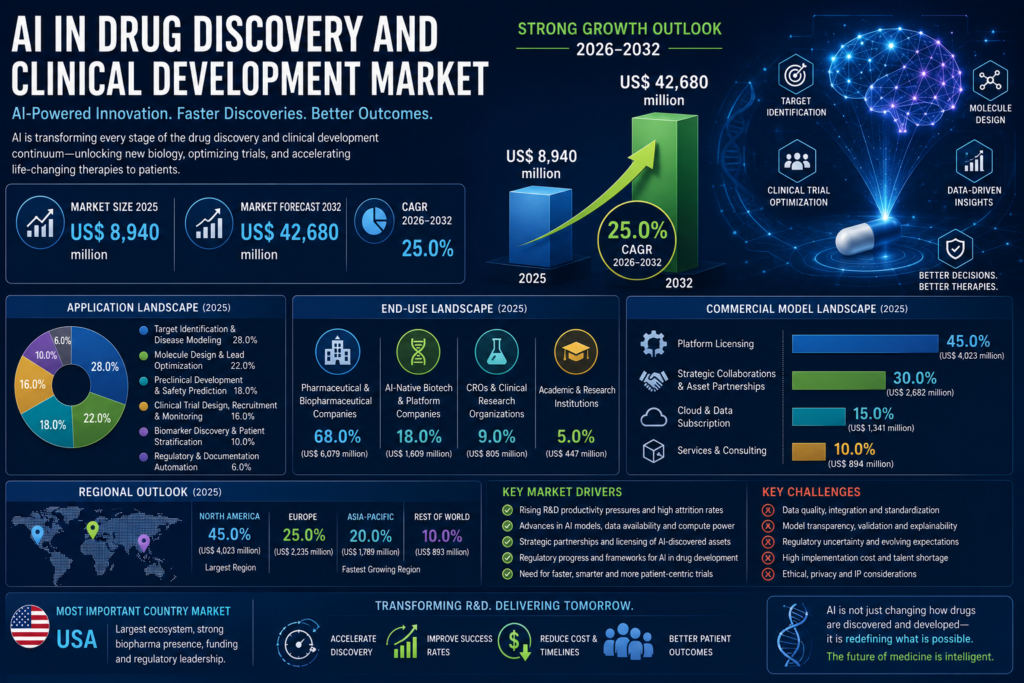

Market Size and Forecast 2032

The AI in Drug Discovery and Clinical Development Market refers to the use of artificial intelligence, machine learning, generative models, foundation models, knowledge graphs, digital biology platforms, large language models, multimodal clinical data systems, and predictive analytics to improve the discovery, optimization, preclinical evaluation, clinical trial design, regulatory preparation, and development execution of medicines. The market includes AI-enabled target identification, molecule generation, protein structure prediction, lead optimization, biomarker discovery, patient stratification, clinical trial recruitment, protocol design, safety monitoring, clinical study report drafting, regulatory evidence generation, and portfolio decision support. It excludes general hospital AI, medical imaging AI used only for diagnosis, manufacturing automation without R&D relevance, and commercial sales analytics not directly linked to drug discovery or clinical development.The global AI in Drug Discovery and Clinical Development Market was valued at US$ 8,940 million in 2025 and is projected to reach US$ 42,680 million by 2032, registering a modeled CAGR of 25.0% during 2026-2032.

Growth is being driven by large pharmaceutical companies embedding AI into R&D operations, the rise of AI-native biotech platforms, major licensing and discovery collaborations, increased use of multimodal clinical datasets, and regulatory movement toward defined frameworks for AI-supported submissions. The market remains early relative to total pharmaceutical R&D spending, but it is shifting from experimentation into operational deployment across discovery, development, and regulatory workflows.

The commercial case for AI in drug discovery and clinical development is strongest where pharmaceutical R&D is constrained by high attrition, long cycle times, complex biology, rising trial costs, and inefficient documentation. AI tools are being used to prioritize targets, generate new chemical matter, predict molecular behavior, identify patient subgroups, optimize trial design, automate literature and evidence review, and accelerate development documentation. FDA has recognized increased use of AI across the drug product life cycle, including nonclinical, clinical, postmarketing and manufacturing phases, and CDER reported more than 500 drug submissions with AI components from 2016 to 2023.

The market is becoming commercially significant because AI is no longer viewed only as a discovery tool. In early adoption, most investment focused on computational chemistry and target discovery. The current phase is broader. Large pharmaceutical companies are building AI-enabled discovery centers, running multimodal data partnerships, implementing LLM-based clinical documentation systems, and collaborating with AI-native companies to generate or license therapeutic assets. Merck and Mayo Clinic announced a 2026 collaboration to apply AI, advanced analytics, multimodal clinical data, genomic datasets and platform architecture to support drug discovery and development, which reflects the shift toward clinically grounded AI systems rather than isolated in silico modeling.

What is changing structurally is the connection between AI-generated insight and clinical development execution. The industry’s early AI promise was speed in discovery. The next stage is whether AI can improve probability of success, reduce avoidable trial failure, shorten administrative delays, and make development decisions faster. FDA’s April 2026 real-time clinical trial initiative is especially important because it shows regulatory interest in using AI and data science to improve trial monitoring, endpoint visibility, safety signal access, and development continuity.

Market Scope

| Metric | Value |

| Market Size in 2025 | US$ 8,940 million |

| Market Size in 2032 | US$ 42,680 million |

| CAGR 2026-2032 | 25.0% |

| Largest Application in 2025 | Target Identification and Disease Modeling |

| Fastest-Growing Application | Clinical Trial Design, Recruitment and Monitoring |

| Largest End Use in 2025 | Pharmaceutical and Biopharmaceutical Companies |

| Fastest-Growing End Use | AI-Native Biotech and Platform Companies |

| Largest Commercial Model in 2025 | Platform Licensing |

| Fastest-Growing Commercial Model | Strategic Collaborations and Asset Partnerships |

| Largest Region in 2025 | North America |

| Fastest Strategic Growth Region | Asia-Pacific |

| Most Important Country Market | USA |

| Key Strategic Trend | Shift from discovery-only AI toward full R&D workflow integration |

| Highest Strategic Priority Theme | Improving R&D productivity while maintaining regulatory-grade model credibility |

Analyst View

The AI in Drug Discovery and Clinical Development Market should be interpreted as an R&D productivity market, not simply a software market. The value is not in whether an algorithm can generate a molecule in isolation. The value is in whether AI can help pharmaceutical organizations make better portfolio decisions, reduce experimental waste, prioritize higher-confidence targets, design molecules with better developability, identify responsive patient groups, and shorten development bottlenecks without compromising scientific rigor.The deeper structural shift is that AI adoption is moving closer to regulated decision-making. FDA’s January 2025 draft guidance provides recommendations for AI used to produce information or data intended to support regulatory decisions regarding drug safety, effectiveness or quality, using a risk-based credibility assessment framework. This matters because the market’s next phase will depend on whether sponsors can validate AI models, document context of use, monitor model performance, and explain outputs clearly enough for regulatory and scientific review.

Commercial value is shifting toward companies that combine proprietary data, biology depth, clinical validation, computational infrastructure, and workflow integration. AI-native platforms can generate candidates and discovery hypotheses, but large pharmaceutical companies control many of the most valuable data assets, development capabilities, regulatory teams, and global clinical operations. This is why partnership models are becoming central. Isomorphic Labs’ collaborations with Eli Lilly and Novartis have potential value of nearly US$ 3,000 million, while Insilico Medicine’s 2026 global R&D collaboration with Lilly includes US$ 115 million upfront and potential total value of approximately US$ 2,750 million.

Market Drivers

Pressure to Improve Pharmaceutical R&D Productivity

The strongest driver is the persistent productivity challenge in pharmaceutical R&D. Drug discovery and development remain expensive, slow, and failure-prone, with many candidates failing before or during clinical testing. AI is commercially attractive because it can improve decision quality earlier in the process by helping scientists identify disease-relevant targets, optimize molecules, evaluate translational biomarkers, and identify likely sources of clinical failure. Merck’s KERMT model, developed with Nvidia and trained on more than 11 million molecules, illustrates how large pharmaceutical companies are applying AI to small-molecule lead optimization to predict molecule behavior earlier and reduce avoidable laboratory cycles.Large Pharmaceutical Partnerships Are Validating the Commercial Model

A second major driver is the scale of strategic partnerships between large pharmaceutical companies and AI-native discovery platforms. These agreements validate AI not only as an internal productivity tool but also as a source of asset creation and licensing economics. Insilico’s March 2026 collaboration with Lilly covers novel therapeutics across multiple therapeutic areas, grants Lilly exclusive worldwide rights to selected oral therapeutic programs, and includes potential total value of approximately US$ 2,750 million. These structures are important because they move AI companies from software vendors toward asset-generation and risk-sharing partners.Clinical Development Bottlenecks Are Creating Demand Beyond Discovery

The third driver is the growing use of AI in clinical development operations. Clinical trials require patient identification, protocol design, site selection, monitoring, medical writing, safety review, endpoint assessment, and regulatory documentation. AI can support patient matching, trial feasibility, real-time monitoring, adverse-event review, clinical study report drafting, and decision support. Merck reported in 2025 that its generative-AI-powered platform reduced first-draft clinical study report creation time from two to three weeks to three to four days and lowered average human-reviewed CSR draft effort from 180 hours to 80 hours.Market Restraints

Model Credibility and Regulatory Acceptance Remain Critical Barriers

The most important restraint is the need for credible, validated, and explainable AI models. Drug development decisions require evidence quality that can withstand regulatory review, scientific challenge, and internal governance scrutiny. AI outputs that cannot be explained, reproduced, audited, or linked to a defined context of use may have limited value in regulated development. FDA’s AI guidance and CDER’s AI governance activities show that regulatory expectations are becoming more structured, which will benefit strong platforms but raise the entry bar for weaker tools.Data Quality, Ownership and Integration Problems Slow Deployment

A second restraint is the uneven quality and accessibility of biomedical and clinical data. Many pharmaceutical datasets remain fragmented across legacy systems, external partners, electronic health records, trial vendors, laboratories, imaging systems, and proprietary research environments. AI performance depends heavily on high-quality, well-annotated, representative data. Poor metadata, biased patient datasets, inconsistent assay outputs, and weak integration between discovery and clinical systems can reduce model reliability and slow enterprise adoption.Clinical Proof of AI-Derived Medicines Is Still Limited

The third restraint is that the industry still needs more clinical proof that AI-originated or AI-optimized candidates can consistently outperform conventional discovery approaches. Insilico’s rentosertib Phase IIa results are an important proof-of-concept milestone for generative AI-enabled drug discovery, but broad market confidence will require more replicated clinical successes across disease areas, modalities, and companies. Investors, pharmaceutical partners, and payers will increasingly distinguish between platforms that generate attractive discovery narratives and platforms that produce candidates with durable clinical and regulatory value.Segmentation Analysis

By Application

Target Identification and Disease Modeling generated US$ 2,350 million in 2025, representing 26.3% of total market revenue, and is projected to reach US$ 9,700 million by 2032. This segment leads because target selection remains one of the highest-value decisions in pharmaceutical R&D. AI models can integrate genomics, proteomics, transcriptomics, spatial biology, real-world data, literature, imaging, and pathway information to identify disease drivers and prioritize intervention points. The segment is especially important in oncology, immunology, neuroscience, metabolic disease, rare disease, and renal disease, where biological complexity and patient heterogeneity create high attrition risk.Molecular Design and Lead Optimization generated US$ 1,980 million in 2025, representing 22.1% of total market revenue, and is projected to reach US$ 9,100 million by 2032. This segment includes generative chemistry, protein and antibody design, ADME prediction, toxicity prediction, ligand optimization, binding prediction, and multi-parameter molecule design. It is commercially important because it can shorten design-make-test-analyze cycles and improve the quality of candidates entering preclinical development. Isomorphic Labs, Insilico Medicine, Recursion, Merck, Sanofi, and other companies are investing heavily in this part of the market because molecule design is one of the clearest areas where computational performance can be linked to measurable productivity gains.

Preclinical and Translational Analytics generated US$ 1,290 million in 2025, representing 14.4% of total market revenue, and is projected to reach US$ 5,100 million by 2032. This segment includes AI-enabled toxicology prediction, biomarker identification, translational modeling, animal-to-human extrapolation, omics interpretation, imaging analytics, and pharmacology modeling. Its role is strategically important because many drug failures occur when preclinical promise does not translate into human efficacy or safety. AI can improve translational confidence by connecting biological mechanism, patient subgroup, biomarker signal, and dose-response evidence earlier in development.

Clinical Trial Design, Recruitment and Monitoring generated US$ 2,050 million in 2025, representing 22.9% of total market revenue, and is projected to reach US$ 11,880 million by 2032, making it the fastest-growing application. This segment includes protocol optimization, trial feasibility, site selection, patient matching, synthetic and external control support, endpoint modeling, digital biomarker analytics, safety monitoring, and real-time trial oversight. FDA’s April 2026 real-time clinical trial initiative with AstraZeneca and Amgen proof-of-concept trials is commercially important because it validates the direction of AI-enabled trial monitoring and continuous data visibility.

Regulatory, Medical Writing and Development Documentation generated US$ 1,270 million in 2025, representing 14.2% of total market revenue, and is projected to reach US$ 6,900 million by 2032. This segment is gaining strategic importance because documentation is one of the largest operational burdens in clinical development. AI systems are now being applied to clinical study reports, regulatory summaries, literature review, safety narratives, submission content, protocol drafting, and quality checks. Merck’s internal generative AI platform provides a practical example of how development documentation can become a measurable AI productivity use case.

By End Use

Pharmaceutical and Biopharmaceutical Companies generated US$ 4,720 million in 2025, representing 52.8% of total market revenue, and are projected to reach US$ 21,500 million by 2032. This segment leads because large drug developers control major R&D budgets, proprietary datasets, clinical operations, compound libraries, and regulatory submission processes. Their AI investments increasingly span discovery, development, medical writing, safety, portfolio governance, and external partnerships. Novartis’ 2026 San Diego research center, expected to house about 1,000 employees and include AI-enabled discovery capabilities, illustrates how AI is being embedded into physical R&D infrastructure rather than treated only as a digital layer.AI-Native Biotech and Platform Companies generated US$ 1,740 million in 2025, representing 19.5% of total market revenue, and are projected to reach US$ 8,400 million by 2032. This segment includes companies that use AI as a core discovery engine, asset-generation model, or integrated drug creation platform. Recursion, Insilico Medicine, Isomorphic Labs, Xaira Therapeutics, Generate:Biomedicines, and similar firms represent this category. The segment is growing quickly because AI-native companies can monetize through licensing, co-development, platform partnerships, pipeline ownership, and milestone economics.

CROs and Clinical Technology Providers generated US$ 1,540 million in 2025, representing 17.2% of total market revenue, and are projected to reach US$ 9,000 million by 2032. This segment is commercially important because clinical development workflows are increasingly outsourced, technology-enabled, and data-intensive. CROs and clinical technology providers are adopting AI for protocol design, trial feasibility, patient recruitment, site performance prediction, medical monitoring, data cleaning, safety signal detection, and decentralized trial support. Their growth is driven by sponsors seeking faster execution without building every AI capability internally.

Academic, Hospital and Research Consortia generated US$ 940 million in 2025, representing 10.5% of total market revenue, and are projected to reach US$ 3,780 million by 2032. This segment includes major hospitals, academic medical centers, translational research networks, and public-private research initiatives. Its importance is rising because multimodal clinical data and longitudinal patient datasets are becoming essential for AI-enabled target discovery, patient stratification, and translational validation. The Merck and Mayo Clinic collaboration reflects how hospital-grade clinical data and genomic datasets are becoming commercially valuable inputs for AI-driven R&D.

By Commercial Model

Platform Licensing generated US$ 3,200 million in 2025, representing 35.8% of total market revenue, and is projected to reach US$ 13,700 million by 2032. This model leads because many pharmaceutical organizations begin AI adoption through access to software platforms, computational chemistry tools, knowledge graphs, target discovery systems, data analytics engines, and workflow automation tools. Platform licensing is attractive because it offers recurring revenue, relatively scalable deployment, and integration into existing R&D functions. However, license renewal increasingly depends on measurable scientific productivity rather than user adoption alone.Strategic Collaborations and Asset Partnerships generated US$ 2,180 million in 2025, representing 24.4% of total market revenue, and are projected to reach US$ 12,200 million by 2032, making it the fastest-growing commercial model. This segment includes co-discovery, co-development, milestone-based licensing, asset generation, and exclusive therapeutic-area partnerships. It is growing rapidly because large pharmaceutical companies increasingly want access not only to AI tools but also to AI-generated therapeutic candidates. The Lilly and Insilico collaboration and Isomorphic’s Lilly and Novartis partnerships illustrate how AI platform companies are moving toward asset-linked economics.

SaaS and Analytics Subscriptions generated US$ 1,660 million in 2025, representing 18.6% of total market revenue, and are projected to reach US$ 7,900 million by 2032. This model includes cloud-based analytics, trial recruitment platforms, clinical operations intelligence, medical writing automation, safety analytics, literature intelligence, and decision-support tools. The model is attractive for clinical development and operational use cases because buyers can adopt tools by function, team, trial, or therapeutic area. Growth will be strongest where AI tools integrate directly into validated workflows and quality systems.

Internal Enterprise AI and Data Infrastructure generated US$ 1,900 million in 2025, representing 21.3% of total market revenue, and is projected to reach US$ 8,880 million by 2032. This segment includes internal AI models, private cloud infrastructure, data lakes, secure model environments, knowledge management systems, computing partnerships, and proprietary foundation models. The segment is strategically important because large pharmaceutical companies increasingly view AI as a core operating capability. Merck’s internal generative-AI platform and KERMT model highlight how major pharma companies are developing owned systems rather than relying only on external vendors.

Regional Analysis

North America AI in Drug Discovery and Clinical Development Market

North America generated US$ 4,800 million in 2025, representing 53.7% of global market revenue, and is projected to reach US$ 20,800 million by 2032. The region leads because it combines the world’s largest pharmaceutical R&D base, strong venture funding, leading AI infrastructure companies, major academic medical centers, deep biotechnology clusters, and an active regulatory environment for AI in drug development. The U.S. is the primary revenue driver, supported by pharmaceutical headquarters, AI-native biotech formation, large clinical trial networks, and early adoption of cloud and generative AI systems.The region’s strategic advantage is not only capital depth. It is the density of the ecosystem. Pharmaceutical companies, academic hospitals, regulators, AI infrastructure providers, computational biology companies, and clinical technology firms are clustered around Boston, San Francisco, San Diego, New York, Seattle, Research Triangle Park, and other major life sciences centers. FDA’s evolving AI guidance and real-time clinical trial initiative create additional momentum by giving sponsors clearer signals about where AI can support regulated development.

USA AI in Drug Discovery and Clinical Development Market

The USA generated US$ 4,210 million in 2025 and is projected to reach US$ 18,190 million by 2032. It is the most important country market because it combines major pharmaceutical R&D spending, leading AI-native biotech companies, extensive clinical trial activity, large electronic health record datasets, advanced regulatory engagement, and strong venture and public-market funding. The U.S. also hosts many of the partnerships and infrastructure investments shaping the market, including Merck’s AI collaborations, Novartis’ AI-enabled San Diego research center, and FDA’s real-time clinical trial proof-of-concept initiative.The U.S. market will remain the largest monetization base because AI tools can be deployed across discovery, clinical operations, regulatory documentation, and trial monitoring at scale. However, buyers will become more demanding. Procurement will increasingly require proof that AI improves cycle time, candidate quality, decision confidence, documentation quality, or clinical execution rather than merely offering computational novelty.

Europe AI in Drug Discovery and Clinical Development Market

Europe generated US$ 2,160 million in 2025, representing 24.2% of global market revenue, and is projected to reach US$ 9,050 million by 2032. Europe is a major market because of its strong pharmaceutical base, academic science, biobanks, national healthcare datasets, and computational biology talent. The U.K., Germany, France, Switzerland, Denmark, Sweden, and the Netherlands are key contributors. Europe’s strengths are particularly visible in structural biology, clinical data access, real-world evidence, and public-private research frameworks.European growth will be shaped by data governance, privacy rules, reimbursement-linked evidence standards, and regulatory alignment. AI adoption will likely be strong in target discovery, clinical trial feasibility, real-world data analytics, and patient stratification. The region’s challenge is scaling AI across fragmented healthcare systems while maintaining privacy, interoperability, and regulatory trust.

Germany AI in Drug Discovery and Clinical Development Market

Germany generated US$ 620 million in 2025 and is projected to reach US$ 2,420 million by 2032. Germany is important because of its pharmaceutical manufacturing base, academic research depth, hospital systems, biomedical engineering capabilities, and growing digital health infrastructure. AI adoption is strongest in translational research, preclinical modeling, clinical data analytics, and drug development partnerships.German growth will depend on secure data-sharing models, integration with hospital networks, and evidence that AI can support high-quality biomedical research without compromising privacy or scientific rigor. Pharmaceutical and medtech convergence will also support AI adoption in clinical development and biomarker-driven trials.

France AI in Drug Discovery and Clinical Development Market

France generated US$ 430 million in 2025 and is projected to reach US$ 1,780 million by 2032. France is a strategically relevant market because of its pharmaceutical base, national health data resources, AI policy support, hospital research networks, and strong mathematics and computational science talent. Growth is expected in clinical development analytics, real-world evidence generation, oncology research, immunology, and regulatory documentation workflows.The French market will remain shaped by public healthcare data governance and national innovation funding. Adoption will be strongest where AI tools can demonstrate patient-level research value, improve trial feasibility, and support development efficiency without weakening oversight.

Asia-Pacific AI in Drug Discovery and Clinical Development Market

Asia-Pacific generated US$ 1,980 million in 2025, representing 22.1% of global market revenue, and is projected to reach US$ 12,830 million by 2032, making it the fastest strategic growth region. Growth is being driven by China’s AI and biotech ecosystem, Japan’s pharmaceutical R&D base, South Korea’s clinical trial infrastructure, India’s data and software talent, and Singapore’s biomedical innovation programs. The region is becoming more important not only as a clinical trial location but also as a source of AI-native discovery platforms and computational biology companies.Asia-Pacific’s growth will be uneven. China has the strongest scale potential due to large patient populations, strong AI investment, rapid biotech formation, and expanding clinical trial activity. Japan has high-quality pharmaceutical R&D and hospital data capabilities but slower enterprise transformation. South Korea has strong digital infrastructure and trial execution capability, making it attractive for AI-enabled clinical development and translational analytics.

Japan AI in Drug Discovery and Clinical Development Market

Japan generated US$ 520 million in 2025 and is projected to reach US$ 3,200 million by 2032. Japan is strategically attractive because of its high-quality pharmaceutical companies, aging-population research needs, strong clinical practice standards, and growing interest in AI-enabled precision medicine. Japanese adoption is likely to focus on target discovery, clinical development efficiency, rare disease research, oncology, neuroscience, and real-world data analytics.Japan’s main challenge will be modernization of data infrastructure and integration across institutional systems. Products and platforms that support explainability, regulatory-grade documentation, and secure clinical data use will be best positioned.

China AI in Drug Discovery and Clinical Development Market

China generated US$ 890 million in 2025 and is projected to reach US$ 6,080 million by 2032. China is one of the fastest-growing country markets because it combines large patient datasets, strong AI talent, expanding biotechnology investment, active clinical development, and rising pharmaceutical innovation. AI-native companies such as Insilico Medicine have helped position the region as a major contributor to AI-enabled discovery and development.China’s market will be shaped by domestic regulatory requirements, cross-border data controls, hospital data access, and pricing pressure. However, the scale of clinical data and speed of platform development make China one of the most important long-term markets for AI-driven translational research and clinical trial optimization.

South Korea AI in Drug Discovery and Clinical Development Market

South Korea generated US$ 170 million in 2025 and is projected to reach US$ 860 million by 2032. South Korea is a smaller but strategically attractive market because of its advanced hospital systems, strong clinical trial infrastructure, digital health adoption, and growing biotech ecosystem. AI adoption is expected to be strongest in oncology, immunology, biomarker analytics, clinical recruitment, and real-world data applications.South Korea’s competitive advantage is execution quality. The country can support high-quality clinical studies, digital patient workflows, and rapid technology integration. Growth will depend on reimbursement-linked evidence, partnerships with global pharma, and local AI-biotech commercialization.

Competitive Analysis

The AI in Drug Discovery and Clinical Development Market is fragmented at the application layer but becoming more concentrated around companies with proprietary datasets, validated platforms, strong partnerships, and clinical-stage pipelines. The competitive field includes AI-native biotechnology companies, large pharmaceutical companies building internal AI engines, cloud and computing providers, CROs, clinical technology platforms, academic hospital networks, and specialized vendors focused on chemistry, biology, trials, safety, or documentation.Competition is increasingly defined by evidence rather than platform claims. In 2021-2023, many companies competed on model architecture, discovery speed, and partnership announcements. By 2026, buyers are demanding stronger proof of impact: clinical candidates, validated targets, improved documentation timelines, reduced trial delays, better patient recruitment, more accurate safety monitoring, and clearer regulatory compliance. Insilico’s rentosertib Phase IIa publication and Merck’s measured clinical study report productivity gains are examples of the type of outcome-based evidence the market increasingly values.

The market is also becoming more collaborative. Large pharmaceutical companies are unlikely to outsource core R&D strategy entirely, but they will continue partnering with AI-native platforms where external systems offer better data, better models, or faster asset generation. At the same time, AI-native companies need pharma partners for late-stage development, regulatory strategy, manufacturing, commercialization, and global market access. This creates a hybrid competitive model where many companies are both partners and competitors.

Key Companies

Recursion

Recursion is one of the most visible AI-native drug discovery companies, especially after its 2024 combination with Exscientia. The combined company described a vertically integrated technology-enabled discovery platform, more than 10 clinical and preclinical programs, around 10 advanced discovery programs, more than 10 partnered programs, and more than US$ 450 million in upfront and realized milestone payments from partners.The company’s strategic direction is centered on industrializing discovery through proprietary data generation, phenomics, chemistry, machine learning, and iterative experimental feedback. Recursion’s importance in this market comes from its attempt to build a scaled discovery engine rather than a single-tool software product. Its future commercial position will depend on clinical readouts, partnership economics, and whether its integrated platform can produce differentiated medicines at a higher success rate than conventional discovery.

Insilico Medicine

Insilico Medicine is a leading AI-native drug discovery company with a strong position in generative AI, target discovery, molecule design, and clinical-stage asset creation. Its rentosertib program in idiopathic pulmonary fibrosis is strategically important because the company reported Phase IIa results published in Nature Medicine, describing the candidate as developed through its generative AI platform and positioned as an early proof-of-concept clinical validation of AI-driven drug discovery.The company’s commercial model combines internal pipeline development, platform partnerships, and licensing. Its March 2026 global collaboration with Lilly is particularly significant because it gives Lilly exclusive worldwide rights to selected preclinical oral therapeutics and includes multiple R&D programs using Insilico’s Pharma.AI platform, with potential total value of approximately US$ 2,750 million. This positions Insilico as both a platform company and an asset generator.

Isomorphic Labs

Isomorphic Labs is one of the most strategically important AI drug design companies because of its connection to Google DeepMind’s scientific infrastructure and the broader AlphaFold ecosystem. Its collaborations with Eli Lilly and Novartis have potential value of nearly US$ 3,000 million, excluding potential royalties, and focus on multi-target small-molecule discovery.The company’s strategic direction is centered on digital biology and AI-driven drug design. Its competitive strength comes from deep model development, structural biology expertise, and high-profile pharmaceutical partnerships. Isomorphic remains commercially important because it represents the convergence of frontier AI research and pharmaceutical asset creation. Its long-term position will depend on whether its platform can progress internally or partnered candidates into clinical validation and regulatory pathways.

Merck

Merck is a major pharmaceutical adopter of AI across discovery and clinical development. The company’s KERMT model, developed with Nvidia and trained on more than 11 million molecules, is focused on improving small-molecule lead optimization by predicting molecule behavior earlier in discovery. Merck has also implemented generative AI tools in clinical development documentation, reporting meaningful reductions in clinical study report drafting time and error rates.Merck’s strategic direction is focused on integrating AI into core R&D rather than using it only as an external innovation layer. Its 2026 collaboration with Mayo Clinic strengthens this position by connecting Merck’s AI and machine learning capabilities with Mayo Clinic’s clinical, genomic, multimodal and platform data assets. This makes Merck a strong example of how large pharma companies are building proprietary AI-enabled R&D infrastructure.

Sanofi

Sanofi is a relevant large-pharma player because it is positioning AI across discovery, clinical development, manufacturing, portfolio decision-making, and collaboration models. The company has publicly described AI as a way to accelerate drug discovery, clinical development, and personalized care, and it has emphasized the role of AI in biologics and complex antibody design.Sanofi’s collaboration with Formation Bio and OpenAI is strategically important because it focuses on customized AI agents and models for pharmaceutical development, with Formation Bio bringing technology platforms and processes built to accelerate drug development and clinical trials. Sanofi’s commercial relevance comes from its ability to apply AI across both internal R&D and external partnership structures, particularly where clinical development execution is the bottleneck.

Key Developments

- In April 2026, FDA announced major steps toward real-time clinical trials, including two proof-of-concept trials that report endpoints and data signals to the agency in real time and a planned pilot program. This matters because it signals regulatory movement toward AI and data science-enabled trial oversight, faster safety signal access, and reduced phase-to-phase development delays.

- In March 2026, Insilico Medicine announced a global R&D collaboration with Lilly using Insilico’s AI engine to accelerate discovery and development of novel therapeutics across multiple therapeutic areas. The agreement includes US$ 115 million upfront and potential total value of approximately US$ 2,750 million, making it one of the clearest recent validations of asset-linked AI drug discovery economics.

- In March 2026, Merck described KERMT, its AI foundation model for small-molecule lead optimization, developed with Nvidia and trained on more than 11 million molecules. This matters because it shows how major pharmaceutical companies are building internal AI models for core medicinal chemistry decisions rather than relying only on external platforms.

- In February 2026, Merck and Mayo Clinic announced a research and development collaboration using AI, advanced analytics, multimodal clinical data, genomic datasets, and Mayo Clinic Platform architecture to support drug discovery and precision medicine. This is significant because clinically grounded multimodal data are becoming one of the most valuable assets in AI-enabled R&D.

- In February 2026, Novartis broke ground on a new global Biomedical Research center in San Diego with AI-enabled discovery capabilities, expected to house about 1,000 employees and form part of a US$ 23,000 million U.S. investment in R&D and advanced manufacturing. This matters because it shows AI being incorporated into long-term physical research infrastructure and global discovery operations.

Conclusion

The AI in Drug Discovery and Clinical Development Market is positioned for rapid expansion through 2032 as pharmaceutical R&D moves from tool-based experimentation to integrated AI-enabled operating models. The largest near-term value pool will remain in target discovery, disease modeling, molecule design and platform licensing, because these areas are already embedded in many discovery organizations. However, the strongest strategic growth will come from clinical trial design, recruitment, monitoring, regulatory documentation, and real-time development analytics, where AI can directly reduce operational friction and shorten development timelines.The market’s next phase will be defined by clinical and regulatory proof. AI platforms that can generate promising preclinical candidates will remain valuable, but the highest valuations and partnership economics will concentrate around companies that can show clinical proof-of-concept, improve development efficiency, and produce evidence acceptable to regulators. FDA’s risk-based AI credibility framework and real-time clinical trial initiative are likely to make model governance, validation, transparency and context-of-use documentation more important commercial differentiators.

By 2032, the market is expected to be more consolidated, more evidence-driven, and more deeply embedded into pharmaceutical decision-making. North America should remain the largest market because of its concentration of pharma R&D, AI infrastructure, biotech capital, and regulatory engagement. Asia-Pacific should grow fastest because of China’s AI-biotech scale, Japan’s high-quality pharmaceutical research base, and South Korea’s advanced clinical infrastructure. The companies best positioned to win will be those that combine proprietary data, validated models, clinical-stage evidence, regulatory credibility, scalable partnerships, and the ability to improve decisions across the full drug discovery and clinical development value chain.