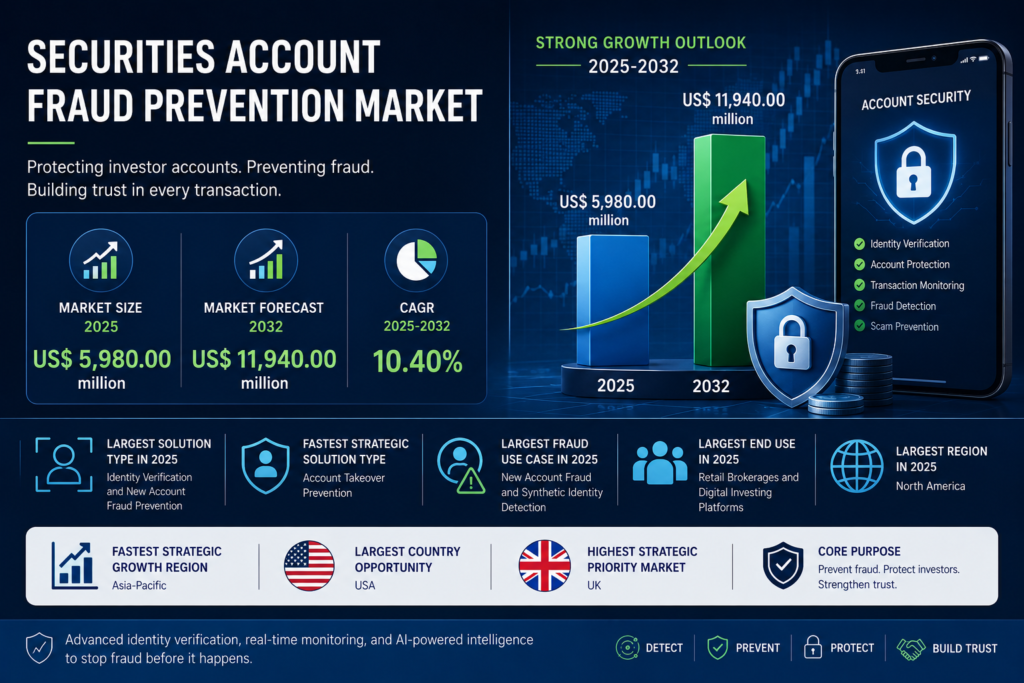

Market Size and Forecast 2032

Securities account fraud prevention covers the technologies, controls, and operating workflows used to detect, prevent, and mitigate fraud across brokerage, mutual fund, and investment advisory accounts. In practical terms, the market includes identity proofing, document and biometric verification, account-takeover defense, device intelligence, behavioral biometrics, transaction anomaly detection, scam intervention, and case-management platforms used to protect customer assets at account opening and throughout the account lifecycle. This is a commercially meaningful category because SEC identity-theft rules apply to brokers, dealers, investment companies, and investment advisers, and the rules explicitly define brokerage, mutual fund, and investment advisory accounts as covered account types that require written programs to detect, prevent, and mitigate identity theft. The global Securities Account Fraud Prevention Market at US$ 5,980.00 million in 2025 and projects it to reach US$ 11,940.00 million by 2032, reflecting a modeled CAGR of 10.40% during 2026-2032. The market remains commercially attractive because it sits at the intersection of three durable demand drivers. The first is the persistence of account takeover risk across online financial accounts. The FBI said that since January 2025 it had received more than 5,100 complaints related to account takeover fraud via impersonation of financial institution support, with losses exceeding US$262 million. The second is rising supervisory attention. FINRA’s 2026 Regulatory Oversight Report includes dedicated sections on Cybersecurity and Cyber-Enabled Fraud and Anti-Money Laundering, Fraud and Sanctions, while the SEC said its Cyber and Emerging Technologies Unit was launched to combat misconduct involving AI, account takeovers, and cybersecurity in securities markets. The third is the need for more layered defenses as AI-enabled fraud rises. The Federal Reserve says account takeover is likely to remain a continued challenge and recommends a layered approach to detection and prevention.

Market Scope

| Metric | Value |

| Market Size in 2025 | US$ 5,980.00 Million |

| Market Size in 2032 | US$ 11,940.00 Million |

| CAGR 2026-2032 | 10.40% |

| Largest Solution Type in 2025 | Identity Verification and New Account Fraud Prevention |

| Fastest Strategic Solution Type | Account Takeover Prevention |

| Largest Fraud Use Case in 2025 | New Account Fraud and Synthetic Identity Detection |

| Largest End Use in 2025 | Retail Brokerages and Digital Investing Platforms |

| Largest Region in 2025 | North America |

| Fastest Strategic Growth Region | Asia-Pacific |

| Largest Country Opportunity | USA |

| Highest Strategic Priority Market | UK |

Analyst View

This market should be interpreted as a trust, access, and transaction-control market, not merely as an authentication market. The strongest demand is appearing where brokerages and wealth platforms need to stop fraud before the account is opened, before the user session is hijacked, and before funds leave the platform. That is why identity proofing, device trust, behavioral analytics, and scam intervention are increasingly being bought together rather than as isolated point tools. The regulatory backdrop reinforces that shift. FINRA’s January 2026 fraud-protection notice proposed broader tools to protect all investors from suspected fraud, including a new Rule 2166 that would permit a temporary delay of up to five business days on disbursements or transactions where there is a reasonable belief of fraud. A second structural shift is the growing importance of AI-aware fraud controls. Sift says account takeover became one of the fastest-growing fraud threats in 2025, with projected losses of US$17 billion and AI-driven tactics such as deepfakes, credential stuffing, and fraud-as-a-service kits helping accelerate attacks. LexisNexis Risk Solutions says 36% of fraud in its digital identity network is now first-party fraud, 85% of identity-fraud cases involve generative AI, and collaboration across organizations increases fraud-detection rates by 43%. These signals matter because securities firms increasingly face a blended threat environment involving synthetic identities, device spoofing, social engineering, and AI-enabled impersonation rather than one isolated fraud vector.Market Drivers

Identity-proofing requirements at account opening are becoming more stringent

Because brokerage and advisory accounts are explicitly covered under SEC identity-theft rules, firms need programs that detect and mitigate identity theft both during account opening and across existing accounts. That requirement is pushing more spending into document verification, biometric proofing, device checks, and synthetic-identity detection at the front end of the customer journey.Account takeover is now a board-level and regulator-level issue

The FBI’s ATO alert, the Federal Reserve’s guidance on layered ATO controls, and FINRA’s 2026 focus on cyber-enabled fraud all point in the same direction: online account compromise is no longer an edge problem for digital channels. It is a core customer-asset protection issue for financial institutions and investment platforms.Fraud-prevention platforms are becoming more networked and intelligence-led

NICE Actimize’s January 2026 launch of Insights Network was positioned around real-time counterparty-risk visibility designed to prevent fraud before money moves. Nasdaq Verafin’s 2026 Global Financial Crime Report said illicit financial activity reached US$4.4 trillion in 2025 and fraud losses exceeded US$500 billion worldwide, highlighting why firms increasingly want shared signals and ecosystem intelligence rather than institution-by-institution detection alone.Market Restraints

False-positive management remains a commercial constraint

Brokerages and wealth platforms cannot simply increase friction at every login or transfer step without damaging acquisition, retention, and client experience. The Federal Reserve’s ATO guidance recommends a layered approach precisely because single-control strategies can miss fraud or create unnecessary customer friction. This means vendors that can combine risk precision with low-friction user experience have a structural advantage.Fraud defense is increasingly fragmented across onboarding, access, and transaction stages

Most securities firms still operate multiple controls across KYC, MFA, device checks, transfers, and case management, often from different vendors. FINRA’s 2026 oversight framing around cyber-enabled fraud, AML, sanctions, and third-party risk highlights how interconnected these control layers have become. In practice, fragmented fraud stacks can slow response time and complicate investigations.AI strengthens both offense and defense

SEC enforcement leadership explicitly said the Cyber and Emerging Technologies Unit was created in part to address misconduct involving AI and account takeovers, while Ping Identity said AI is accelerating identity-based attacks and that stronger biometric re-verification is needed across digital interactions. This means fraud-prevention investment must keep pace with adversaries who now use AI to make impersonation and onboarding fraud more convincing.Market Segmentation Analysis

By Solution Type

Identity Verification and New Account Fraud Prevention generated US$ 1,980.00 million in 2025, representing 33.1% of total market revenue, and is projected to reach US$ 3,760.00 million by 2032. This segment leads because securities firms must establish trust at onboarding before an account is funded or linked for withdrawals. SEC Regulation S-ID makes this especially relevant for brokers, investment companies, and advisers, and IDEMIA Public Security and Indicio’s March 2026 financial-services launch shows how biometric proofing, document verification, and portable verified identity are moving into more interoperable deployment models. Account Takeover Prevention generated US$ 1,420.00 million in 2025 and is projected to reach US$ 3,220.00 million by 2032. This is the fastest strategic segment because ATO risk increasingly spans login abuse, session hijacking, support impersonation, and step-up re-verification. The FBI’s complaint data, the Federal Reserve’s ATO guidance, BioCatch’s DeviceIQ launch, and Ping Identity’s Keyless integration all support the rising importance of this category. Transaction Monitoring and Behavioral Analytics generated US$ 1,060.00 million in 2025 and is projected to reach US$ 2,120.00 million by 2032. This segment remains commercially important because many fraud events are only obvious when activity is viewed in context, such as a change in profile followed quickly by a large transfer request. The Federal Reserve’s example of triggering additional verification when a user changes address and then tries to transfer half the account balance illustrates why behavioral and event-chain analysis matter. Authentication, Biometrics and Step-Up Security generated US$ 860.00 million in 2025 and is projected to reach US$ 1,680.00 million by 2032. This segment is growing because deepfakes, impersonation, and device spoofing are weakening older static controls. Ping Identity’s January 2026 Keyless integration added zero-knowledge biometrics and rapid re-verification for anti-spoofing and anti-ATO use cases, while IDEMIA and Indicio’s joint solution emphasizes high-assurance, privacy-preserving identity verification for financial services. Case Management, Orchestration, Anti-Phishing and Channel Defense generated US$ 660.00 million in 2025 and is projected to reach US$ 1,160.00 million by 2032. This segment remains smaller than onboarding and ATO, but it is strategically important because phishing, scam coaching, and cross-channel impersonation increasingly sit upstream of account compromise. FINRA’s proposed fraud “speed bump” and trusted-contact enhancements show why firms need intervention workflows, not only detection tools.By Fraud Use Case

New Account Fraud and Synthetic Identity Detection generated US$ 1,760.00 million in 2025, representing 29.4% of total market revenue, and is projected to reach US$ 3,260.00 million by 2032. This segment leads because fraudulent securities accounts create downstream losses across funding, transfers, trading, and customer remediation. SEC covered-account rules and IDEMIA’s March 2026 financial-services launch both reinforce the importance of stronger onboarding controls. Account Takeover and Credential Abuse Prevention generated US$ 1,520.00 million in 2025 and is projected to reach US$ 3,440.00 million by 2032. This segment is rising quickly because the industry increasingly faces phishing, support impersonation, malware, and AI-enhanced credential attacks. FBI complaint data and BioCatch’s DeviceIQ launch both highlight how persistent this problem has become. Withdrawal, Transfer and Cash-Out Fraud Detection generated US$ 1,160.00 million in 2025 and is projected to reach US$ 2,280.00 million by 2032. This segment remains critical because the final monetization point for many fraud attacks is a disbursement or transfer out of the account. FINRA’s proposed Rule 2166, which would permit temporary delays for suspected fraud affecting investors of any age, directly reflects the commercial need to interrupt suspicious outflows before they settle. Insider, Mule and Collusive Fraud Detection generated US$ 860.00 million in 2025 and is projected to reach US$ 1,740.00 million by 2032. This segment is gaining relevance because fraud networks increasingly use mule structures and collaborative schemes rather than simple one-off account theft. LexisNexis says mule networks are a core part of digital fraud and notes an average of 15 mules per uncovered network in its Global State of Fraud and Identity reporting. Investor Protection, Scam and Exploitation Intervention generated US$ 680.00 million in 2025 and is projected to reach US$ 1,220.00 million by 2032. This segment remains smaller today, but it has rising strategic importance because regulators increasingly expect firms to help prevent customer harm, not just detect technical fraud. FINRA’s January 2026 notice explicitly focused on protecting senior investors and all investors from suspected fraud through trusted contacts, temporary holds, and new transaction-delay tools.By End Use

Retail Brokerages and Digital Investing Platforms generated US$ 2,140.00 million in 2025, representing 35.8% of total market revenue, and are projected to reach US$ 4,320.00 million by 2032. This segment leads because digitally opened and digitally serviced brokerage accounts are high-value fraud targets and are directly covered by SEC identity-theft rules. It is also the most exposed to onboarding fraud, account takeover, and digital cash-out activity. Wealth Management and Advisory Firms generated US$ 1,280.00 million in 2025 and are projected to reach US$ 2,480.00 million by 2032. This segment is commercially important because advisory accounts hold significant value and often involve a mix of digital access and human interaction, which increases exposure to impersonation and social engineering. FINRA’s fraud-protection proposals are especially relevant here because advisor-led relationships can still be targeted through disbursement scams and investor exploitation. Banks with Brokerage and Investment Accounts generated US$ 1,220.00 million in 2025 and are projected to reach US$ 2,420.00 million by 2032. This segment remains large because hybrid banking-investment platforms are exposed to account-opening fraud, linked-account abuse, and multi-channel impersonation. The FBI’s ATO alert and BioCatch’s digital-banking device intelligence launch are particularly relevant to this crossover environment. Crypto-Securities and Multi-Asset Investment Platforms generated US$ 760.00 million in 2025 and are projected to reach US$ 1,540.00 million by 2032. This segment is strategically important because multi-asset platforms compress onboarding, funding, and trading into one digital journey, which raises the value of real-time identity, device, and transaction controls. SEC enforcement commentary linking account takeovers and AI-related misconduct to securities transactions supports the relevance of this category. Market Infrastructure, Clearing, Custody and Transfer Providers generated US$ 580.00 million in 2025 and is projected to reach US$ 1,180.00 million by 2032. This segment remains smaller than retail-facing platforms, but it is increasingly important because fraud-prevention responsibility is extending into transfer, settlement, and broader market-operations workflows. FINRA’s 2026 emphasis on protection of customer assets and operational resilience supports this direction.Regional Analysis

Our model identifies North America as the largest region in 2025, supported by the concentration of SEC and FINRA rulemaking, the FBI’s high-profile ATO alerting, and the strongest cluster of active vendor launches from NICE Actimize, BioCatch, and Ping Identity. Our model identifies Asia-Pacific as the fastest strategic growth region, reflecting the broader spread of digital investment platforms and the relevance of interoperable identity systems across cross-border financial services, an area highlighted by IDEMIA and Indicio’s March 2026 launch.Competitive Landscape

The Securities Account Fraud Prevention Market is fragmented in product architecture but increasingly concentrated around a smaller set of vendors that can combine onboarding intelligence, ATO prevention, transaction-risk scoring, and response orchestration. NICE Actimize, BioCatch, Ping Identity, IDEMIA Public Security, Nasdaq Verafin, and broader identity-and-risk intelligence providers are all relevant, but they compete on different strengths. NICE Actimize is strongest in enterprise fraud orchestration and network intelligence. BioCatch is strongest in behavioral and device intelligence. Ping Identity is increasingly important in identity assurance and biometric re-verification. IDEMIA focuses on high-assurance proofing and portable trusted identity. Nasdaq Verafin contributes intelligence and collaboration framing at the broader financial-crime level. Competition is increasingly shaped by three factors. The first is control-point coverage, meaning how well a platform spans onboarding, login, session, transfer, and recovery stages. The second is signal depth, especially around device, behavior, counterparty, and identity evidence. The third is operational usability, because firms increasingly need not just alerts but actionable workflows that let them pause, verify, escalate, and document fraud decisions in regulated environments.Key Companes

NICE Actimize

NICE Actimize remains one of the most strategically important companies in this market because it is extending fraud prevention from institution-specific monitoring toward network-aware intelligence. In January 2026, it launched the Actimize Insights Network, which it says gives financial institutions real-time visibility into counterparty risk and helps prevent fraud before money moves while supporting governance. Its strength lies in connecting fraud intelligence to decisioning and case handling at scale.BioCatch

BioCatch is strategically important because it sits at the intersection of behavioral intelligence, device intelligence, and account takeover defense. In March 2026, it launched DeviceIQ, a device-identification and intelligence product designed to help financial institutions evaluate the trustworthiness of devices used in digital banking. For securities and wealth platforms, that matters because device trust is becoming a critical signal for both new-account fraud and ongoing ATO prevention.Ping Identity

Ping Identity remains highly relevant because AI-driven impersonation is raising the value of privacy-preserving re-verification. In January 2026, Ping said completion of the Keyless acquisition added zero-knowledge biometrics, device-independent authentication, and re-verification in under 300 milliseconds to strengthen defenses against spoofing, deepfakes, and account takeover. Its strategic value lies in pushing fraud prevention closer to continuous identity assurance rather than one-time login control.IDEMIA Public Security

IDEMIA Public Security is strategically important because it is building toward portable, high-assurance identity that can work across institutions and borders. Its March 2026 partnership with Indicio combined biometric identity proofing, document verification, and verifiable credentials into an interoperable financial-services identity solution explicitly designed to address deepfake and synthetic identity fraud. That makes it particularly relevant in new-account fraud prevention and higher-assurance onboarding environments.Nasdaq Verafin

Nasdaq Verafin remains commercially important because it frames fraud prevention as a collaborative network problem rather than a single-institution analytics problem. In March 2026, its Global Financial Crime Report said illicit activity had reached US$4.4 trillion in 2025 and fraud losses exceeded US$500 billion worldwide, while also emphasizing private-sector collaboration against fraud and scams. Its relevance is strongest where firms want shared intelligence and a broader financial-crime context for fraud prevention strategy.Recent Developments

- In March 2026, BioCatch launched DeviceIQ, a device-identification and intelligence product aimed at helping financial institutions assess device trustworthiness in digital banking. This was commercially meaningful because device intelligence is becoming a core layer in both onboarding and account-takeover defense.

- In March 2026, IDEMIA Public Security and Indicio launched an interoperable financial-services identity-verification solution combining biometric proofing, document verification, and verifiable credentials with explicit protection against deepfake and synthetic identity fraud. This matters because securities-account fraud prevention is moving toward portable, standards-based, higher-assurance identity.

- In January 2026, NICE Actimize launched the Actimize Insights Network, positioning it as a real-time intelligence layer that helps institutions prevent fraud before money moves. This matters because shared counterparty-risk intelligence is becoming increasingly valuable in transfer and cash-out fraud.

- In January 2026, FINRA proposed broader fraud-protection rule changes, including new Rule 2166 to allow a temporary five-business-day delay on disbursements or transactions when there is a reasonable belief of fraud, plus broader trusted-contact and hold-period changes. This is important because it shows the supervisory framework moving toward more proactive fraud intervention.

- In January 2026, Ping Identity completed the Keyless acquisition, adding zero-knowledge biometrics and rapid re-verification to strengthen defenses against AI-powered spoofing, impersonation, and account takeover. This reflects the rising importance of biometric and step-up security in higher-risk account events.