Market Overview

The global Semiconductor-Grade Nitric Acid Market includes ultra-pure nitric acid used in semiconductor wafer cleaning, silicon etching, polysilicon etching, aluminum wet etching, electronic materials preparation, flat panel display processing, photovoltaic production, LED fabrication, MEMS, compound semiconductors, and advanced electronics manufacturing. The market covers electronic-grade, semiconductor-grade, ultra-high-purity, low-metal, low-particle, SEMI-aligned, and customer-specific fab-qualified nitric acid supplied in bulk, drums, totes, containers, custom blends, and closed chemical delivery systems. It excludes fertilizer-grade, industrial-grade, laboratory reagent, explosives-grade, and general metal-treatment nitric acid where semiconductor-level impurity, particle, packaging, and process qualification standards are not required.Semiconductor-grade nitric acid is commercially important because it functions as a strong oxidizing acid in wet etching, surface preparation, and cleaning processes. UBE describes its high-purity nitric acid as a refined product developed for the electronics industry and positioned for cleaning and etching silicon wafers. Agilent notes that nitric acid plays an important role in semiconductor device fabrication, with nitric and hydrofluoric acid mixtures used to etch single-crystal silicon and polycrystalline silicon, while nitric, phosphoric and acetic acid combinations are used for aluminum wet etching.

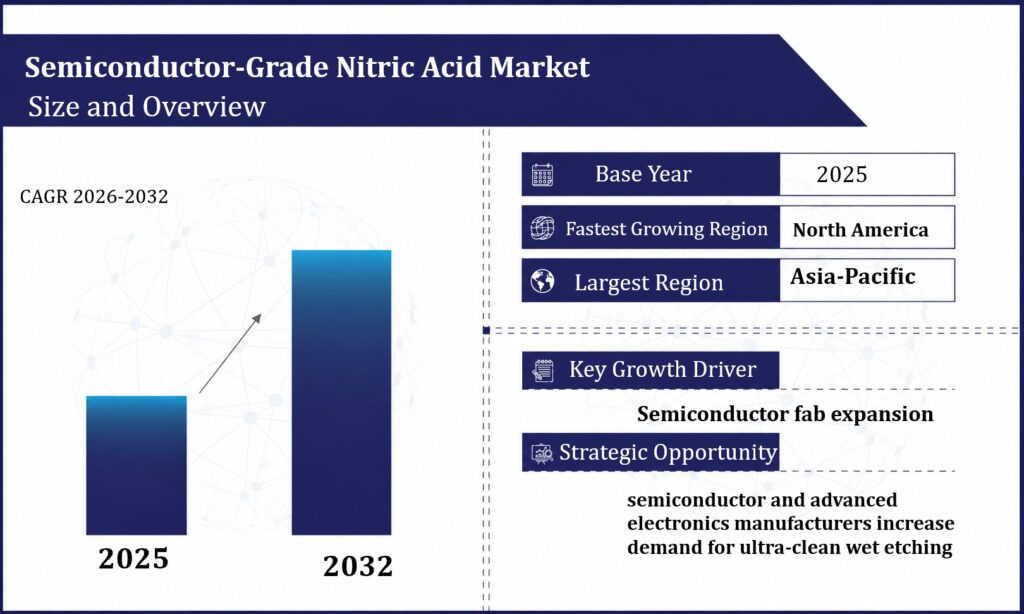

The global Semiconductor-Grade Nitric Acid Market was valued at US$ 684.6 million in 2025 and is projected to reach US$ 1,326.8 million by 2032, registering a modeled CAGR of 9.9% during 2026-2032.Growth is being driven by 300mm fab expansion, wafer cleaning demand, silicon and polysilicon wet etching, display manufacturing, MEMS processing, power semiconductor production, photovoltaic cell manufacturing, and increasing need for ultra-low-metal wet chemicals. Worldwide 300mm fab equipment spending is expected to increase 18.0% to US$ 133.0 billion in 2026 and 14.0% to US$ 151.0 billion in 2027, supported by AI chip demand, data centers, edge devices, and regional semiconductor self-sufficiency programs.

The market is structurally different from industrial nitric acid because value is determined by impurity control, particle control, packaging cleanliness, concentration consistency, and fab qualification. Advanced semiconductor applications require nitric acid with very low metal contamination because trace elements can influence wafer defects, etch behavior, and device reliability. High-purity chemical suppliers and wafer fabs increasingly rely on trace metal impurity analysis for semiconductor process chemicals, especially as advanced manufacturing pushes contamination limits lower.

The market is structurally different from industrial nitric acid because value is determined by impurity control, particle control, packaging cleanliness, concentration consistency, and fab qualification. Advanced semiconductor applications require nitric acid with very low metal contamination because trace elements can influence wafer defects, etch behavior, and device reliability. High-purity chemical suppliers and wafer fabs increasingly rely on trace metal impurity analysis for semiconductor process chemicals, especially as advanced manufacturing pushes contamination limits lower.

A major structural shift is the movement toward regional and fab-qualified supply. Wet chemicals used in semiconductor fabrication are essential across cleaning, etching, and surface preparation, and their availability, purity, and performance are critical to manufacturing yield and reliability. Broader semiconductor wet chemicals and specialty cleans demand remains on a growth path, with industry coverage reporting 5.0% shipment growth to 2,706 million kg and 6.0% revenue growth to US$ 5,440.0 million in 2025.

Executive Market Snapshot

| Metric | Value |

| Market Size in 2025 | US$ 684.6 million |

| Market Size in 2032 | US$ 1,326.8 million |

| CAGR 2026-2032 | 9.9% |

| Largest Grade Type in 2025 | Semiconductor Ultra-High-Purity Nitric Acid |

| Fastest-Growing Grade Type | Customized Low-Metal Fab-Qualified Nitric Acid |

| Largest Application in 2025 | Silicon Wafer Cleaning and Etching |

| Fastest-Growing Application | Advanced Packaging and Surface Preparation |

| Largest Distribution Model in 2025 | Direct Fab Bulk Supply |

| Fastest-Growing Distribution Model | Regional Localized Supply Hubs |

| Largest Region in 2025 | Asia-Pacific |

| Fastest Strategic Growth Region | North America |

| Most Important Country Opportunity | Taiwan |

| Highest Strategic Priority Theme | Ultra-low-metal nitric acid supply for controlled wet etching and wafer surface preparation |

Analyst Perspective

The Semiconductor-Grade Nitric Acid Market should be viewed as a contamination-control and etch-performance market rather than a commodity acid market. Nitric acid is a mature chemical, but semiconductor-grade nitric acid becomes a high-value process material only when it is purified, filtered, packaged, stored, and delivered with extremely low metals and particles. Fabs do not evaluate it only by acid strength. They evaluate it by etch behavior, lot consistency, metallic impurity levels, residue profile, packaging cleanliness, and compatibility with qualified wet process recipes.The strongest value pool remains silicon and polysilicon etching. Nitric acid is used with hydrofluoric acid in silicon etch chemistry, where nitric acid acts as an oxidizing component and HF removes the formed oxide. This application supports semiconductor wafers, MEMS, sensors, photovoltaic cells, and specialty silicon processing. Aluminum etching is another important use case because nitric acid can be part of phosphoric acid and acetic acid mixtures used in aluminum wet etch processes.

The second major value shift is toward low-metal and customer-specific grades. As device dimensions shrink and wafer surface requirements tighten, nitric acid suppliers must provide stronger impurity documentation, more controlled packaging, and tailored concentration or blend specifications. Custom blending is also becoming more relevant because some customers require nitric acid diluted or combined with other acids to reach targeted etch rates for specific materials.

Strategic decision-makers should view this market as steady but qualification-heavy. Nitric acid is not always the largest wet chemical by volume, but it is process-critical where oxidation-driven etching, metal etching, and surface preparation are required. Suppliers with high-purity distillation, low-metal analytics, cleanroom packaging, local warehousing, and fab qualification experience will capture stronger value than suppliers selling standard acid grades.

Market Dynamics

Market Drivers

Semiconductor fab expansion is increasing high-purity wet chemical demand

The strongest driver is global fab expansion. Every new or expanded fab requires high-purity acids, bases, oxidizers, solvents, etchants, and surface preparation chemicals. SEMI’s 2026 and 2027 outlook points to a major 300mm investment cycle, with spending expected to reach US$ 133.0 billion in 2026 and US$ 151.0 billion in 2027. This directly supports demand for semiconductor-grade nitric acid used in wet etching, cleaning, and electronics processing.Silicon and polysilicon etching sustain core process demand

Nitric acid remains important in silicon and polysilicon etching, particularly in nitric acid and hydrofluoric acid mixtures. These chemistries are used where controlled silicon removal is required in semiconductor, MEMS, photovoltaic, and specialty wafer processing. Agilent identifies nitric acid as important in semiconductor fabrication and notes its use in HF-nitric acid mixtures for etching single-crystal and polycrystalline silicon.Aluminum wet etching and specialty electronics support diversified demand

Nitric acid also supports aluminum wet etching in mixtures containing phosphoric acid and acetic acid. This gives the market exposure to semiconductor metallization, display processing, MEMS, sensors, power electronics, and specialty electronics. UBE’s positioning of high-purity nitric acid for silicon wafer cleaning and etching shows the chemical’s broad role in electronics manufacturing rather than only one process step.Market Restraints

Ultra-high-purity production raises cost and limits supplier participation

The largest restraint is the cost of producing semiconductor-grade nitric acid. Suppliers must manage raw material quality, distillation, filtration, metal impurity testing, particle control, clean packaging, compatible containers, and hazardous acid logistics. These requirements create higher costs than industrial nitric acid and limit the number of producers capable of serving advanced fabs.Nitric acid is highly hazardous and requires strict handling

Nitric acid is strongly oxidizing and corrosive. High-purity grades require not only safe handling but also contamination-free handling. Fabs and suppliers must manage acid-compatible packaging, ventilation, temperature control, operator safety, spill response, transportation controls, and clean chemical transfer. This increases total delivered cost and operational complexity.Process substitution can limit demand in selected applications

Nitric acid is important, but it competes with dry etching, alternative wet etchants, peroxide-based cleans, plasma processes, and formulated specialty chemicals depending on the material stack. In advanced semiconductor manufacturing, process selection depends on selectivity, defectivity, surface damage, etch rate, and integration strategy. This means nitric acid growth is linked to specific wet etching and cleaning requirements rather than total wafer starts alone.Market Segmentation Analysis

By Grade Type

Semiconductor Ultra-High-Purity Nitric Acid generated US$ 248.6 million in 2025, representing 36.3% of total market revenue, and is projected to reach US$ 462.8 million by 2032. This segment leads because wafer fabs require nitric acid with very low metallic impurities, controlled particles, and stable concentration for cleaning, etching, and surface preparation. It is used in semiconductor, MEMS, display, photovoltaic, and specialty electronics production where process contamination must be tightly managed.Electronic Grade Nitric Acid generated US$ 142.8 million in 2025, representing 20.9% of total market revenue, and is projected to reach US$ 246.6 million by 2032. This segment serves displays, mature-node semiconductors, solar cells, LEDs, PCB-adjacent electronics, and general electronic manufacturing that requires higher purity than industrial acid but not always the tightest advanced-node specifications. Electronic-grade nitric acid suppliers position the material for semiconductor and advanced electronics use with ultra-low metal contamination and precise concentration control.

UP-S and UP-SS Grade Nitric Acid generated US$ 124.6 million in 2025, representing 18.2% of total market revenue, and is projected to reach US$ 264.8 million by 2032. These grades serve customers that require lower metals and particles than general electronic grade, including power devices, image sensors, specialty wafer processing, mature logic, and display lines. Growth is supported by the shift from broad electronic-grade chemicals toward more tightly controlled impurity profiles.

UP-SSS and SEMI-Aligned Nitric Acid generated US$ 96.8 million in 2025, representing 14.1% of total market revenue, and is projected to reach US$ 214.6 million by 2032. This segment supports advanced fabs and high-reliability electronics where chemical specifications are aligned with strict customer and semiconductor materials standards. The segment benefits from increased trace-metal testing and the need for stronger documentation across critical wet processes.

Customized Low-Metal Fab-Qualified Nitric Acid generated US$ 71.8 million in 2025, representing 10.5% of total market revenue, and is projected to reach US$ 137.9 million by 2032, making it the fastest-growing grade type. This category includes customer-specific nitric acid grades with customized concentration, trace-metal limits, particle controls, container formats, acid blends, and closed-transfer compatibility. Custom chemical formulations using high-purity nitric acid are used where customers require targeted etch rates on certain materials.

by Application

Silicon Wafer Cleaning and Etching generated US$ 246.4 million in 2025, representing 36.0% of total market revenue, and is projected to reach US$ 468.6 million by 2032. This application leads because high-purity nitric acid is used for cleaning and etching silicon wafers. UBE specifically identifies its high-purity nitric acid as suitable for cleaning and etching silicon wafers, which supports its central role in wafer processing.Silicon and Polysilicon Etching with HF-Nitric Acid Blends generated US$ 146.8 million in 2025, representing 21.4% of total market revenue, and is projected to reach US$ 286.5 million by 2032. This segment includes etch chemistries where nitric acid and hydrofluoric acid are used together to etch single-crystal silicon and polycrystalline silicon. It is important in semiconductor wafers, MEMS, sensors, photovoltaic cells, and specialty silicon processing.

Aluminum and Metal Etching generated US$ 92.6 million in 2025, representing 13.5% of total market revenue, and is projected to reach US$ 174.8 million by 2032. This segment includes aluminum wet etch mixtures and selected metal-surface treatment processes. Nitric acid is used with phosphoric and acetic acid for aluminum wet etching, supporting demand in semiconductor metallization, display panels, MEMS, and specialty electronics.

Display Panel and LCD Processing generated US$ 78.4 million in 2025, representing 11.5% of total market revenue, and is projected to reach US$ 138.6 million by 2032. This application includes LCD, OLED, glass substrate, and flat panel display processing where high-purity acids are used in cleaning, etching, and surface conditioning. Stella Chemifa describes its high-purity chemical agents as used for cleaning and etching in semiconductor and liquid crystal panel manufacturing processes.

Photovoltaic, LED and Specialty Electronics Processing generated US$ 68.6 million in 2025, representing 10.0% of total market revenue, and is projected to reach US$ 124.8 million by 2032. This segment includes solar cells, LEDs, MEMS, SiC, GaN, sensors, and specialty electronic components. Demand is smaller than silicon wafer processing but supported by the wider use of high-purity chemicals in advanced electronics.

Advanced Packaging and Surface Preparation generated US$ 51.8 million in 2025, representing 7.6% of total market revenue, and is projected to reach US$ 133.5 million by 2032, making it the fastest-growing application. Advanced packaging requires low-contamination surface preparation, metal compatibility, residue control, and selective treatment for redistribution layers, wafer-level packaging, and hybrid integration. Growth is supported by AI accelerators, chiplets, HBM, and 2.5D or 3D packaging.

by Distribution Model

Direct Fab Bulk Supply generated US$ 284.6 million in 2025, representing 41.6% of total market revenue, and is projected to reach US$ 526.4 million by 2032. This model leads because high-volume fabs and display manufacturers need stable, qualified nitric acid supply with reliable documentation and traceability. Direct supply supports bulk tanks, quality agreements, process-change control, and emergency response.High-Purity Specialty Chemical Distribution generated US$ 132.4 million in 2025, representing 19.3% of total market revenue, and is projected to reach US$ 238.6 million by 2032. This channel serves specialty fabs, research lines, MEMS producers, display makers, photovoltaic manufacturers, and smaller electronics users. Distribution value comes from safe acid handling, documentation, smaller packaging, and regional availability.

Drum and Tote Supply generated US$ 96.8 million in 2025, representing 14.1% of total market revenue, and is projected to reach US$ 172.6 million by 2032. This model supports mid-volume users that require high-purity acid but not full bulk tank supply. High-purity nitric acid is often distributed in drums, one-way totes, returnable totes, and specialized containers depending on customer volume and logistics needs.

Custom Acid Blending and Dilution generated US$ 72.6 million in 2025, representing 10.6% of total market revenue, and is projected to reach US$ 146.8 million by 2032. This segment includes custom nitric acid blends with hydrofluoric acid, phosphoric acid, acetic acid, or other strong acids for targeted etching and process-specific chemical behavior. Many applications require high-purity nitric acid to be diluted or blended to reach desired solution specifications.

Closed Transfer and On-Site Chemical Management generated US$ 58.6 million in 2025, representing 8.6% of total market revenue, and is projected to reach US$ 126.8 million by 2032. This model includes closed containers, chemical cabinets, compatible transfer lines, point-of-use filtration, and on-site acid management. Growth is driven by the need to preserve purity from supplier packaging to process tool.

Regional Localized Supply Hubs generated US$ 39.6 million in 2025, representing 5.8% of total market revenue, and are projected to reach US$ 115.6 million by 2032, making it the fastest-growing distribution model. Localized hubs reduce freight risk, support emergency supply, shorten lead times, and improve customer support near major fab clusters. This model is gaining importance in Taiwan, South Korea, Japan, China, Singapore, the USA, and Germany.

Regional Analysis

North America Semiconductor-Grade Nitric Acid Market

North America generated US$ 96.4 million in 2025 and is projected to reach US$ 246.8 million by 2032, making it the fastest strategic growth region. Growth is being driven by U.S. fab localization, advanced packaging, specialty electronics, and domestic high-purity wet chemical supply. The region is also supported by local chemical distribution and custom blending capabilities for high-purity nitric acid used in electronics and semiconductor applications.USA Semiconductor-Grade Nitric Acid Market

The USA generated US$ 84.8 million in 2025 and is projected to reach US$ 224.6 million by 2032. The USA is the core North American opportunity because fabs in Arizona, Texas, New York, Ohio, Oregon, Idaho, and related electronics clusters require qualified wet chemicals for cleaning, etching, surface preparation, and advanced packaging. Demand will depend on fab ramp schedules, supplier qualification, local warehousing, and safe high-purity acid logistics.Europe Semiconductor-Grade Nitric Acid Market

Europe generated US$ 78.6 million in 2025 and is projected to reach US$ 146.8 million by 2032. Europe’s demand is supported by power semiconductors, automotive electronics, specialty fabs, MEMS, sensors, displays, and regional semiconductor material localization. Germany, France, Ireland, Italy, Belgium, and the Netherlands are important markets. Growth is quality-led rather than purely volume-led.Germany Semiconductor-Grade Nitric Acid Market

Germany generated US$ 24.8 million in 2025 and is projected to reach US$ 48.6 million by 2032. Germany’s demand is tied to automotive semiconductors, power devices, Dresden fab expansion, sensors, and high-reliability electronics. The market favors suppliers that can offer strong documentation, low-metal impurity control, and safe regional delivery of high-purity wet chemicals.France Semiconductor-Grade Nitric Acid Market

France generated US$ 12.6 million in 2025 and is projected to reach US$ 23.8 million by 2032. France’s market is supported by microelectronics, aerospace electronics, power devices, research fabs, and specialty sensors. Demand is concentrated in quality-sensitive wet processing and specialty electronic materials rather than broad commodity acid use.Asia-Pacific Semiconductor-Grade Nitric Acid Market

Asia-Pacific generated US$ 446.8 million in 2025 and is projected to reach US$ 786.4 million by 2032, making it the largest regional market. The region leads because Taiwan, South Korea, Japan, China, and Singapore host the largest concentration of foundries, memory fabs, display producers, photovoltaic manufacturers, and electronic materials suppliers. Japan is especially important in high-purity nitric acid supply because UBE, Mitsubishi Chemical, Kanto-related suppliers, and other Japanese chemical companies have strong positions in ultra-pure electronics chemicals.Taiwan Semiconductor-Grade Nitric Acid Market

Taiwan generated US$ 126.8 million in 2025 and is projected to reach US$ 224.8 million by 2032. Taiwan is the most important country opportunity because of its advanced foundry ecosystem and large 300mm fab base. Demand is strongest for low-metal nitric acid used in wafer cleaning, silicon etching, metal etching, and advanced surface preparation. Kanto-PPC lists high-purity bulk nitric acid as part of its electronic chemicals portfolio, supporting Taiwan’s regional supply ecosystem.Japan Semiconductor-Grade Nitric Acid Market

Japan generated US$ 96.5 million in 2025 and is projected to reach US$ 168.4 million by 2032. Japan is strategically important because of its deep high-purity chemical capabilities. UBE’s high-purity nitric acid is developed for the electronics industry and used for silicon wafer cleaning and etching. Mitsubishi Chemical also states that its semiconductor materials business creates and sells ultra-high-purity process chemicals for semiconductor and electronic device production, including liquid crystal panels and solar cells.China Semiconductor-Grade Nitric Acid Market

China generated US$ 108.4 million in 2025 and is projected to reach US$ 208.6 million by 2032. China is a major growth market because of domestic wafer fab expansion, display manufacturing, photovoltaic production, PCB processing, and electronic materials localization. The key challenge is maintaining consistent ultra-low-metal quality and achieving qualification for advanced semiconductor processes.South Korea Semiconductor-Grade Nitric Acid Market

South Korea generated US$ 72.8 million in 2025 and is projected to reach US$ 134.8 million by 2032. South Korea’s demand is driven by DRAM, NAND, HBM, displays, and advanced packaging. Memory fabs require repeatable wet chemical performance at high volume, making low-metal acid supply and supplier reliability important procurement priorities.Latin America Semiconductor-Grade Nitric Acid Market

Latin America generated US$ 34.8 million in 2025 and is projected to reach US$ 68.6 million by 2032. Brazil and Mexico are the main markets, primarily through electronics assembly, PCB processing, photovoltaic activity, and specialty chemical distribution. The region remains smaller because advanced wafer fabrication capacity is limited.Middle East and Africa Semiconductor-Grade Nitric Acid Market

Middle East and Africa generated US$ 28.0 million in 2025 and is projected to reach US$ 78.2 million by 2032. Growth is early-stage but supported by electronics localization, solar manufacturing, advanced industrial projects, and selected Gulf technology initiatives. Large-scale demand will depend on whether regional semiconductor and advanced electronics manufacturing reaches commercial scale.Competitive Landscape

The Semiconductor-Grade Nitric Acid Market is moderately concentrated at the ultra-high-purity level and more fragmented in regional electronic chemical distribution. Leading suppliers compete on metal impurity control, distillation technology, concentration consistency, particle reduction, packaging quality, custom blending capability, logistics safety, and fab qualification history.Competition is strongest in Asia-Pacific because the region contains the largest semiconductor and display manufacturing base. Japan holds a strong position in high-purity nitric acid technology and process chemical quality. North America and Europe are becoming more strategically important as fabs and governments push for local supply-chain resilience. The highest-value competition is moving toward customer-specific, low-metal, fab-qualified nitric acid grades rather than standard electronic-grade acid.

By 2032, suppliers that combine ultra-high-purity production, custom acid blending, clean packaging, regional warehousing, safe hazardous logistics, and point-of-use support will hold stronger positions. The market will increasingly reward suppliers that can deliver documented purity and process consistency close to major fabs.

Key Company Profiles

UBE Corporation

UBE Corporation is one of the most relevant suppliers in the market because its high-purity nitric acid is specifically developed for the electronics industry and positioned for cleaning and etching silicon wafers. UBE’s strength lies in refined nitric acid production, electronics-grade process chemical quality, and alignment with Japan’s semiconductor materials ecosystem.Mitsubishi Chemical

Mitsubishi Chemical is strategically relevant through its semiconductor materials business, which creates and sells ultra-high-purity process chemicals for production processes of semiconductors, liquid crystal panels, and solar cells. The company emphasizes chemical purity improvement and development of new chemicals for semiconductor and electronic products.Kanto Chemical and Kanto-PPC

Kanto Chemical and Kanto-PPC are important in high-purity process chemical supply. Kanto Chemical has developed high-purity chemicals and automatic chemical dispense systems for semiconductor manufacturing since 1964. Kanto-PPC lists nitric acid as part of its high-purity bulk chemicals offering for electronic chemical use.Stella Chemifa

Stella Chemifa is relevant through its high-purity chemical business for semiconductor and liquid crystal panel manufacturing. The company states that its high-purity chemical agents are used in cleaning and etching processes for semiconductors and liquid crystal panels. Its position is strongest in Japan’s high-purity chemical ecosystem and advanced electronics materials supply chain.Columbus Chemical Industries

Columbus Chemical Industries is relevant in high-purity nitric acid distribution, dilution, and custom blending. The company supplies high-purity nitric acid in bulk, drums, totes, and returnable containers, and provides custom chemical formulations where customers need targeted etch rates on specific materials. Its role is strongest in North American distribution, specialty packaging, and custom blending.Recent Developments

- In April 2026, SEMI projected worldwide 300mm fab equipment spending to increase 18.0% to US$ 133.0 billion in 2026 and 14.0% to US$ 151.0 billion in 2027. This is directly relevant to semiconductor-grade nitric acid because new fabs require qualified wet chemicals for cleaning, etching, surface preparation, and specialty electronic material processing.

- In 2025, semiconductor wet chemicals and specialty cleans shipments were reported to grow 5.0% to 2,706 million kg, with revenues rising 6.0% to US$ 5,440.0 million. This confirms the broader growth environment for high-purity wet chemicals, including semiconductor-grade nitric acid.

- In 2025, UBE’s high-purity nitric acid continued to be positioned for the electronics industry, with specific use in silicon wafer cleaning and etching. This reinforces Japan’s role in the high-purity nitric acid supply chain for semiconductor and electronics manufacturing.

- In 2025, high-purity chemical suppliers and distributors continued expanding custom nitric acid blending and packaging options, including drums, totes, returnable containers, and acid blends designed for targeted etch-rate requirements. This is commercially important because semiconductor and specialty electronics customers increasingly require process-specific formulations rather than only standard acid grades.

Strategic Outlook

The Semiconductor-Grade Nitric Acid Market is positioned for steady growth through 2032 as semiconductor and advanced electronics manufacturers increase demand for ultra-clean wet etching, silicon surface preparation, and metal etching chemicals. Silicon wafer cleaning and etching will remain the largest application, while advanced packaging and surface preparation will provide the strongest growth as surface cleanliness and metal compatibility become more important in chiplet, HBM, and wafer-level packaging processes.Asia-Pacific will remain the largest region because Taiwan, Japan, South Korea, China, and Singapore dominate semiconductor, display, photovoltaic, and electronic materials production. North America will grow fastest as U.S. fabs expand and regional high-purity chemical supply becomes more strategic. Europe will remain quality-focused, supported by power semiconductors, automotive electronics, sensors, and specialty fabs.

Companies best positioned to win will combine high-purity nitric acid production, low-metal analytics, clean packaging, custom blending, hazardous chemical logistics, and regional fab support. By 2032, semiconductor-grade nitric acid is expected to remain a specialized but strategically important wet chemical category, with value shifting toward customer-specific low-metal grades, localized supply hubs, and controlled acid blends for next-generation electronics manufacturing.